How to Refinance Student Loans with a Low Credit Score in USA: The Complete 2026 Guide

Fact: According to FICO, a credit score below 670 is considered “bad credit” for refinancing purposes. But here is the truth most lenders won’t tell you: You can still refinance with a score below 600 – you just need the right strategy .

If you are one of the 45 million Americans carrying student loan debt (average balance over $39,000), you have probably heard the advice: “Refinance to a lower rate!” . But when you actually check your credit score and see a number closer to 580 than 780, that advice feels like a cruel joke.

Low credit scores lead to higher interest rates. Higher rates mean you pay more over time. But in 2026, new lending products and strategies have emerged specifically for borrowers with damaged credit.

This guide walks you through exactly how to refinance student loans with bad credit – from finding cosigners to leveraging new “partial payment” programs .

Part 1: Understanding the Bad Credit Refinancing Landscape in 2026

Before we get into strategies, you need to understand what lenders are looking for and why bad credit complicates things.

What Is Considered a “Bad” Credit Score?

Credit scores range from 300 to 850. According to FICO, one of the most popular scoring models:

| Credit Score Range | Rating | Refinancing Implication |

|---|---|---|

| 740 – 850 | Excellent | Best rates, automatic approval |

| 670 – 739 | Good | Approval likely, competitive rates |

| 580 – 669 | Fair | Approval possible but rates higher |

| 300 – 579 | Poor | Difficult to refinance alone |

The definition varies by scoring model. VantageScore considers anything below 661 as bad credit . The key takeaway: “bad credit” does NOT mean “no options” – it means you need a different approach.

What Lenders Actually Look At

Your credit score is NOT the only factor. When you apply to refinance student loans, private lenders evaluate :

- Credit Score (30-35% of decision) – Your history of paying debt

- Debt-to-Income Ratio (DTI) – Your monthly debt payments divided by gross monthly income

- Employment History – Stable income over 2+ years is ideal

- Education Level – Some lenders favor advanced degrees

- Cosigner Status – This can override almost all other factors

The Federal vs. Private Loan Trap

Before you refinance ANY federal student loans, understand this critical warning: When you refinance federal loans with a private lender, you permanently lose access to all federal benefits .

This includes:

- Public Service Loan Forgiveness (PSLF)

- Income-Driven Repayment (IDR) plans

- The new Repayment Assistance Plan (RAP) coming in 2026

- Deferment and forbearance options

- Loan discharge programs for disability or death

Only refinance federal loans IF:

- You work in the private sector (no PSLF eligibility)

- Your income is too high for IDR plans

- You have excellent credit and can get a rate under 4%

Part 2: Strategy #1 – The Cosigner Approach (Fastest Path to Approval)

If you have bad credit, finding a cosigner is statistically the most effective way to refinance. A cosigner is someone who legally agrees to pay your loan if you cannot .

Why a Cosigner Works

When you apply with a cosigner who has good credit (700+), the lender evaluates the cosigner’s creditworthiness alongside yours. This significantly increases your approval chances and can unlock much lower interest rates.

Real Example: A borrower with a 580 credit score applies alone. Denied. The same borrower applies with a parent who has a 780 credit score and stable income. Approved at 6.5% APR.

Who Can Be a Cosigner?

Most people ask parents or legal guardians, but you can ask virtually anyone who :

- Is over 18 years old

- Is a US citizen or permanent resident

- Has good credit (700+)

- Has stable income

- Trusts you completely

The Serious Responsibility

Agreeing to cosign a loan is a massive commitment. Here is what your cosigner needs to understand :

- They are equally liable – If you miss a payment, they must pay

- Their credit is on the line – Late payments hurt both your credit scores

- Their debt-to-income ratio increases – This can affect their ability to buy a house or car

- Cosigner release may take years – Most lenders require 24-48 months of on-time payments before releasing a cosigner

How to Ask Someone to Cosign

Before you ask, prepare:

- A realistic budget showing how you will make payments

- Proof of income (recent pay stubs)

- An emergency plan (what happens if you lose your job?)

- A written agreement between you and the cosigner

Be prepared to hear “no” – and respect that answer .

Cosigner Release: The Exit Strategy

Most lenders offer a “cosigner release” option after a certain number of on-time payments. For example, Lake Trust Credit Union allows cosigner release after 48 consecutive on-time payments during the principal and interest repayment period .

Part 3: Strategy #2 – Building Your Credit Before Refinancing

If you cannot find a cosigner, or if you want to refinance alone in the future, improving your credit score is your best long-term strategy.

Check Your Credit Reports for Errors

You can obtain a free copy of your credit report from each of the three major credit bureaus – Equifax, Experian, and TransUnion – at AnnualCreditReport.com .

Common errors that hurt your score:

- Paid-off loans still showing as active

- Accounts that do not belong to you

- Late payments that were actually on time

- Duplicate accounts

Dispute any errors immediately. A single correction can boost your score by 30-50 points.

3 Fastest Ways to Improve Your Credit

1. Make Every Single Payment on Time (35% of your score)

Payment history is the single biggest factor in your credit score. Set up automatic payments (autopay) to ensure you never miss a due date . Some lenders even offer a 0.25% interest rate discount for enrolling in autopay .

2. Pay Down Credit Card Balances (30% of your score)

Credit utilization – how much of your available credit you are using – is the second most important factor. Keep utilization below 30% of your total credit limit. Below 10% is ideal.

3. Stop Applying for New Credit

Every time a lender does a “hard credit check” when you apply for a loan or credit card, your score takes a small temporary hit. Multiple applications in a short period can significantly slow your progress .

Alternative Credit-Building Tools

If you have thin credit (not enough history) rather than bad credit:

- Secured credit cards – You put down a deposit ($200-$500) as your credit limit

- Become an authorized user – Ask a family member to add you to their credit card account

- Credit-builder loans – Small loans from credit unions designed to build history

Improve Your Debt-to-Income Ratio (DTI)

Your DTI is calculated as: Monthly Debt Payments ÷ Gross Monthly Income

To improve your DTI :

- Increase income (side job, negotiate a raise, work overtime)

- Decrease debt (pay off credit cards or small loans first)

- Lower your monthly debt obligations where possible

Lenders prefer a DTI below 40%. Below 30% is excellent.

Part 4: Strategy #3 – Finding Lenders That Work with Bad Credit

Not all lenders have the same credit requirements. Some specialize in working with borrowers who have fair or poor credit.

Credit Unions: The Hidden Gem

Credit unions are nonprofit financial cooperatives that often have more flexible lending standards than large banks .

Advantages of credit unions:

- Lower rates than banks (often 3.90% – 11.50% APR)

- More personal underwriting (they look at your whole financial picture)

- Willing to work with members who have lower scores

Requirements:

- You must become a member (usually $5-$25)

- Many require you to live, work, or study in a specific region

Example: Lake Trust Credit Union offers student loan refinancing with rates starting at 3.90% APR. They allow borrowers to refinance all or some of their loans, and they offer a cosigner release option after 48 on-time payments .

Major Online Lenders (Lower Requirements)

| Lender | Minimum Credit Score (Approx.) | Key Feature |

|---|---|---|

| SoFi | 650 (with cosigner) | SmartStart program – 9 months of interest-only payments |

| Earnest | 650-680 | Customizable terms; soft credit check to pre-qualify |

| Splash Financial | Varies by partner | Rates from 3.71% APR for qualified borrowers |

The Soft Pull vs. Hard Pull Distinction

Before you officially apply, use each lender’s “rate check” tool. These typically use a soft credit pull, which does NOT affect your credit score .

Only when you formally submit a full application does the lender perform a hard credit pull, which temporarily lowers your score by a few points.

Strategy: Check rates with 3-5 lenders using soft pulls. Compare offers. THEN apply with the best one.

Part 5: Alternative Strategies – Refinancing Without Traditional Approval

Nonprofit Debt Consolidation

If you have multiple debts (credit cards, personal loans, PLUS student loans), a nonprofit credit counseling agency can help you consolidate into one manageable payment .

How it works:

- You work with a certified credit counselor

- They negotiate with creditors on your behalf

- You make one monthly payment to the agency

- They distribute payments to your creditors

Pros: Lowers monthly payments, eliminates unsecured debt over time, protects your credit

Cons: Fees apply, only works for unsecured debt, takes years to complete

Secured Loans (High Risk, High Reward)

A secured loan is backed by collateral – something the lender can take if you stop paying, such as your car or home equity .

Example: Using a home equity loan or second mortgage to pay off student loans.

WARNING: This is extremely risky. If you default, you could lose your home. Only consider this if:

- You have significant home equity

- Your income is stable and reliable

- You fully understand the foreclosure risk

SoFi SmartStart: Partial Payments for 9 Months

In 2026, SoFi introduced SmartStart, a refinancing product designed for borrowers who need breathing room .

How it works:

- You pay only interest for the first 9 months (no principal)

- This lowers your initial monthly payment significantly

- After 9 months, you transition to full principal + interest payments

Example: On a $50,000 loan at 6.47% APR, your monthly payment during the first 9 months is approximately $269 (interest only). After 9 months, it increases to approximately $567 (full payment) .

Who qualifies: SoFi’s “most qualified borrowers” – which typically requires a credit score of 650+ or a cosigner.

Part 6: The 2026 Federal Law Changes You Must Know

The One Big Beautiful Bill Act (OBBBA) , signed into law on July 4, 2025, fundamentally changed the federal student loan system . These changes affect whether you should refinance at all.

Key Changes Starting July 1, 2026

| Change | Details | Impact on Refinancing Decision |

|---|---|---|

| Grad PLUS eliminated | Graduate students cannot borrow Grad PLUS loans after 7/1/26 | More graduate students may need private loans (including refinancing) |

| Parent PLUS capped | $20,000/year, $65,000 lifetime limit | Parents may need to refinance existing PLUS loans |

| New RAP plan replaces SAVE | Repayment Assistance Plan has higher payments than SAVE | Federal loans become less attractive for some borrowers |

| SAVE forbearance ending | Interest started accruing August 1, 2025 | Borrowers on SAVE may see balances growing |

The RAP vs. SAVE Comparison

| Provision | RAP (New Plan) | SAVE (Ending) |

|---|---|---|

| Minimum payment | $10 | $0 in some cases |

| Income disregarded | None | First $35,000 |

| Forgiveness timeline | 30 years | 20-25 years |

| Payment on $40k income | ~$132/month | ~$40/month |

What this means: Federal loans are becoming less generous. For borrowers with good credit, refinancing to a private loan with a lower rate may actually be MORE attractive in 2026 than keeping federal loans .

PSLF Is Still Available (For Now)

If you work for a government agency or nonprofit, you can still pursue Public Service Loan Forgiveness. However, recent changes mean :

- Residency and fellowship years no longer count toward the 120 payments

- Employer eligibility is under federal review following a 2025 executive order

- Parent PLUS borrowers must consolidate and enroll in IBR before June 30, 2026 to remain eligible

If you are pursuing PSLF, DO NOT refinance your federal loans. Doing so eliminates your eligibility permanently .

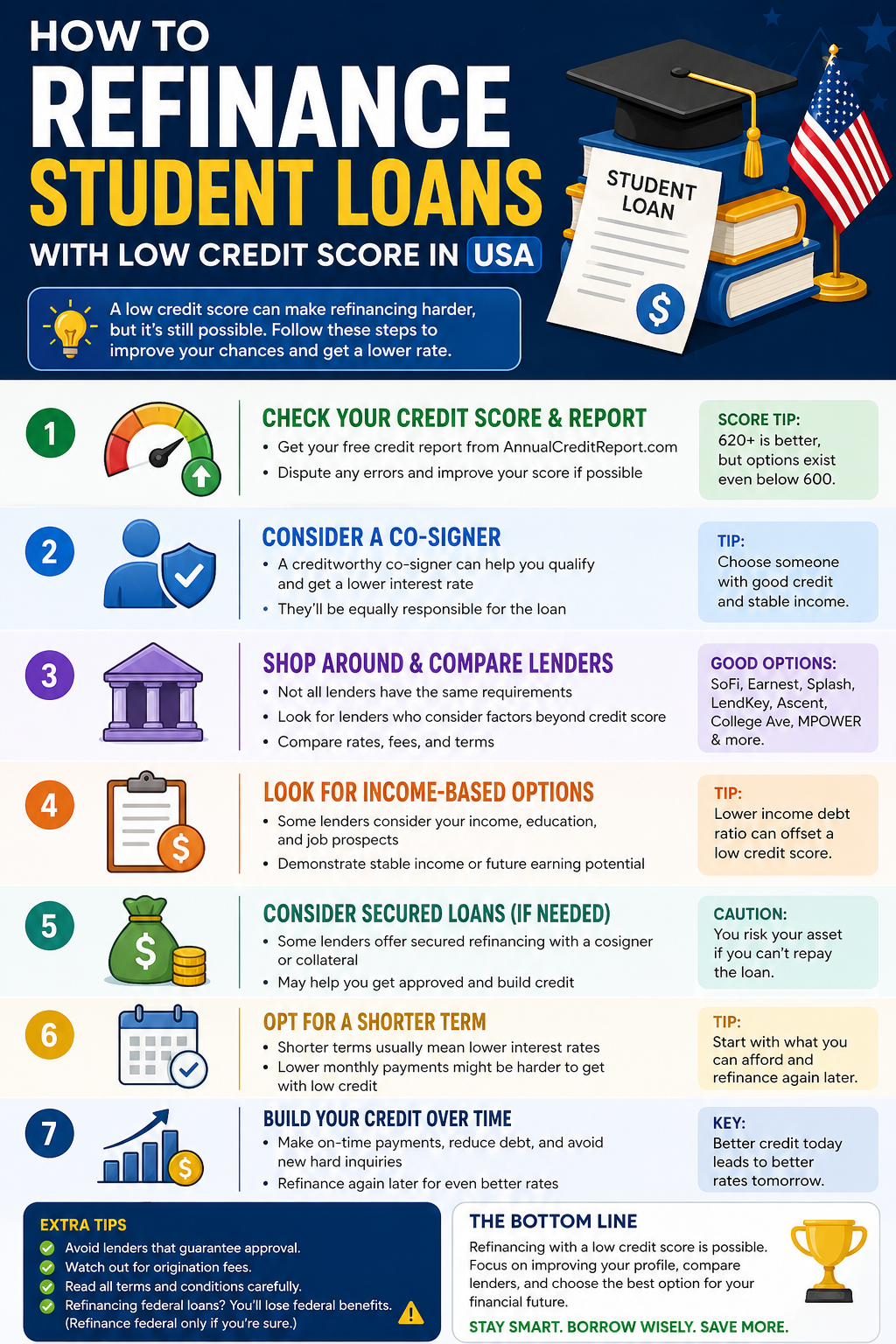

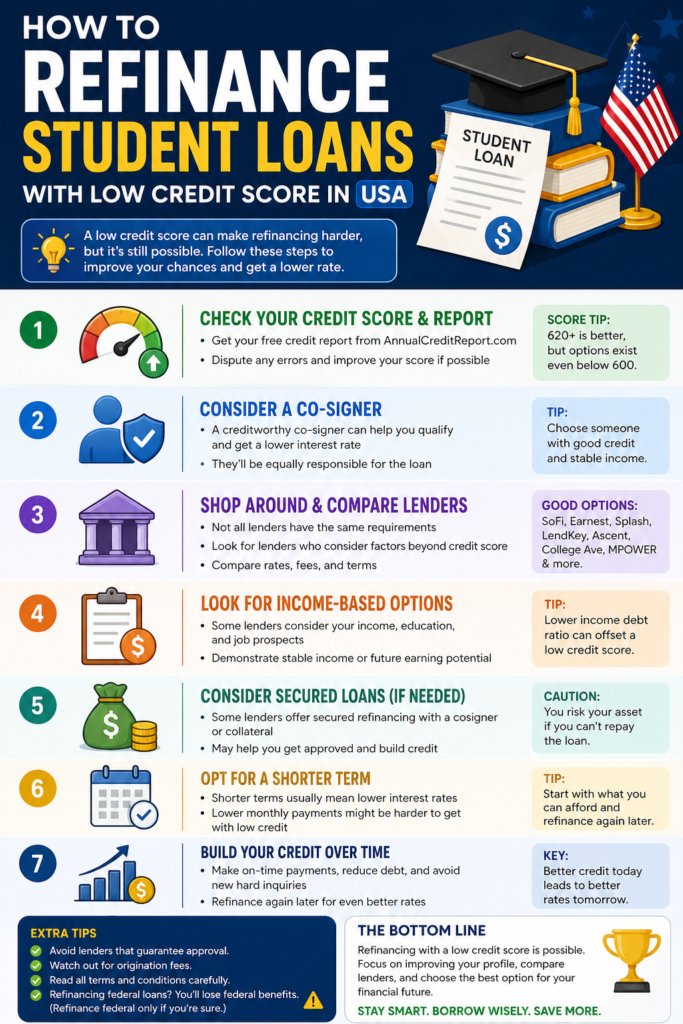

Part 7: Step-by-Step Action Plan for 2026

If You Need to Refinance NOW (Low Credit Score)

Step 1: Pull your credit reports from AnnualCreditReport.com. Dispute any errors.

Step 2: Identify a potential cosigner (parent, relative, trusted friend). Have an honest conversation about expectations.

Step 3: Use soft-pull rate check tools with 3-5 lenders:

- SoFi (SmartStart program for partial payments)

- Earnest (customizable terms)

- Local credit unions (check StudentChoice.org for partners)

Step 4: Compare offers. Choose the lowest APR with terms you can afford.

Step 5: Submit a full application with your cosigner. Complete all documentation.

Step 6: Set up autopay to ensure you never miss a payment. Build toward cosigner release.

If You Can Wait 6-12 Months

Step 1: Focus on credit improvement – on-time payments, paying down credit cards, no new applications.

Step 2: Build emergency savings (3-6 months of expenses) so unexpected costs do not derail loan payments.

Step 3: Every 3 months, do a soft-pull rate check to see if your improving credit has unlocked better offers.

Step 4: Once your score reaches 650+ (or you find a cosigner), apply.

If You Have Federal Loans and Are Considering Refinancing

Step 1: Ask yourself these questions:

- Do I work for a nonprofit or government? → DO NOT REFINANCE (PSLF is worth too much)

- Is my income low relative to my debt? → DO NOT REFINANCE (IDR/RAP plans will help)

- Do I have private loans or high-interest federal loans? → CONSIDER REFINANCING

Step 2: If you decide to refinance, act before July 1, 2028 – after that, all borrowers will be automatically moved to RAP, which has higher payments than current IDR plans .

Part 8: Red Flags and Scams to Avoid

When searching for “student loan refinancing with bad credit,” you will encounter predatory lenders. Avoid anyone who:

- Guarantees approval without checking your credit (legitimate lenders always check)

- Charges upfront fees for refinancing (reputable lenders charge $0 fees)

- Promises “loan forgiveness” for a fee (forgiveness is free through the government)

- Pressures you to refinance federal loans without explaining the loss of benefits

Safe lenders: SoFi, Earnest, Splash Financial, credit unions affiliated with StudentChoice.org .

Summary Table: Your 2026 Refinancing Options by Credit Score

| Credit Score | Best Strategy | Expected APR Range | Timeline |

|---|---|---|---|

| 740+ (Excellent) | Refinance alone | 3.71% – 5.50% | Immediate |

| 670-739 (Good) | Refinance alone or with cosigner | 5.50% – 7.50% | Immediate |

| 580-669 (Fair) | Apply with cosigner OR improve credit for 6-12 months | 7.50% – 11.50% | 1-3 months (with cosigner) |

| 300-579 (Poor) | Credit improvement first (12+ months) OR secured cosigner | 11.50%+ | 12-24 months |

The Bottom Line

Refinancing student loans with a low credit score is challenging but absolutely possible in 2026. Your fastest path is a qualified cosigner . Your smartest long-term path is credit improvement . Your safest path is keeping federal loans if you qualify for PSLF or income-driven plans .

The new OBBBA laws make federal loans less generous starting July 1, 2026, which paradoxically makes private refinancing more attractive for borrowers with good credit or cosigners . But for borrowers with bad credit, the federal safety net (however reduced) may still be your best option.

Check your rates with multiple lenders using soft pulls. Compare offers. Calculate the total interest over the life of the loan. And never refinance federal loans without fully understanding what protections you are giving up.

Your student loan debt does not define your future. A strategic refinancing plan – even with bad credit – can put you on the path to financial freedom.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Interest rates, lender requirements, and federal student loan programs change frequently. All rate examples are estimates and may not reflect actual offers available to you. Always consult with a qualified financial advisor or student loan counselor before refinancing federal student loans or making significant financial decisions.